Nagaland’s spending on health, education lower than North East & Himalayan States

Our Correspondent

Kohima | March 26

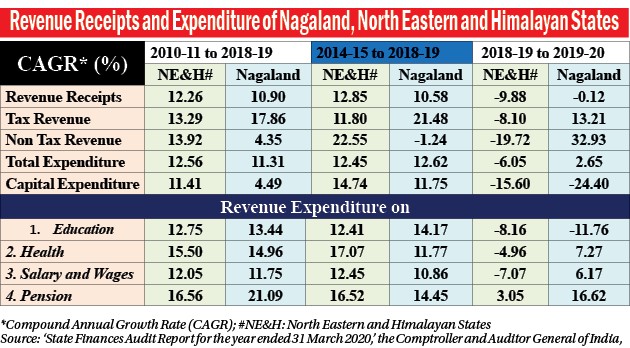

Nagaland share of expenditure on Health (5.% and 5.20% during 2015-16 and 2019-20 respectively) were lower than the averages of North Eastern & Himalayan States (5.95% and 6.19% during 2015-16 and 2019-20 respectively).

This was highlighted in the State Finances Audit Report of the Comptroller and Auditor General of India for the year ended 31st March 2020, tabled at the 11th session of 13th Nagaland Legislative Assembly (NLA) here on March 22.

Similarly, the State's share of expenditure on Education (14.79 and 12.92 per cent during 2015-16 and 2019-20 respectively) as proportion of Aggregate Expenditure was less than that of the averages of North Eastern & Himalayan States (18.32 and 17.42 per cent during 2015-16 and 2019-20 respectively).

As per Finance Accounts 2019-20, the State Government invested Rs 1 crore as equity in Government Company (Nagaland State Mineral Development Corporation Limited.

As on 31 March 2020, whereas the State Government made investment of Rs295.17 crore in Government Companies, Statutory Corporation, Co-operative Societies and Joint Stock Companies, the return on investments was a meager Rs 2.80 crore by way of dividends during the year.

The state had outstanding guarantees of Rs 174.96 crore as on 31 March 2020.

The outstanding Public Debt rapidly increased from Rs 6,736.24 crore (14.26 per cent) from 2015-16 to Rs 9.118.09 crore (35.36 per cent) in 2019-20 whereas the Debt/GSDP ratio decreased from 34.50 per cent to 29.89 per cent during the same period.

The outstanding Public Debt was Rs 8,115.52 crore during 2018-19, which increased by Rs 1,002.57 crore (12.35 per cent) compared to the previous year. About nine to ten per cent of the revenue receipts were used by the State for payment of interest on the outstanding Public Debt and the average rate of interest ranged between 6.15 per cent to 7.29 per cent during last five years period from 2015-16 to 2019-20.

The Report stated that maturity profile of outstanding stock of Public Debt as on 31 March 2020 indicates that out of Outstanding Public Debt of Rs 9,118.09 crore, 47.25 per cent of debt needs to be repaid within seven yeaRs

Revenue deficit of Rs 213.73 crore

Meanwhile, as per the report, Nagaland had a Revenue Deficit of Rs 213.73 crore during 2019-20 which was 0.70 per cent of GSDP.

Fiscal deficit was Rs 1,428.22 crore during 2019-20 which was 4.68% of GSDP and primary deficit was Rs 614.48 crore, 2.01% of GSDP.

The report stated that Revenue Receipts were Rs 11,423.29 crore during 2019-20, which decreased by 14.12 crore (0.12 per cent) compared to the previous year.

During the current year, State's Own Tax and Non-Tax Revenue increased by Rs 112 crore (13.24 per cent) and Rs 84 crore (32.94 per cent) respectively over the previous year.

Grants-in-Aid from Government of India increased by Rs 315.36 crore (4.82 per cent) while State's Share of Union Taxes and Duties decreased by Rs 525.33 crore (13.85 per cent) as compared to the previous year.

Revenue Expenditure accounted for 90.54 per cent of total expenditure during the current year. Committed expenditure like salary and wages, pension, interest payments steadily increased during the last five-year period 2015-20.

The Committed Expenditure during the year 2019-20 was 68.93 per cent of the Revenue Receipts and 67.66 per cent of the Revenue Expenditure.

State Govt short contributed to NPS

Under National Pension System (NPS), the State Government short contributed Rs 30.51 crore resulting in understatement of revenue and fiscal deficit to that extent.

Further, as on 31 March 2020, Rs 170.35 crore were outstanding under NPS, with the State Government and had not been transferred to NSDL, creating avoidable outstanding financial liabilities under the Scheme.

Capital Expenditure is the expenditure for creation of assets of permanent and material character.

Capital Expenditure (Rs 1,206 crore) decreased by 24.44 per cent during 2019-20 compared to the previous year and stood at nine per cent of the total expenditure during the year.

Recommendations

The Report stated that the State Government needs to give greater focus on development expenditure by steadily increasing its Capital expenditure on identified infrastructure gaps in a planned manner with periodical review and monitoring mechanism at the highest level of administration,

The State Government would do well by increasing its expenditure on Health and Education to compare favourably with NE Region States.

To avoid possible future liabilities under NPS, the State Government needs to fulfill their obligation by releasing arrears of its contributions and transferring the outstanding funds already accumulated, to NSDL for management of the NPS.

The State Government may seriously review the functioning of the Corporations, Companies and Societies to ensure returns on their investments and consider either revival or closure of non-functional units, in a time bound manner.

The State Government may ensure that mobilised debt resources are used adequately for incurring capital expenditure for creation of assets. The increasing trends of Revenue Expenditure be corrected by identifying potential wasteful expenditure and adopting economy measures across departments. Own revenues need to be augmented to meet the interest on debt liabilities, the report stated.