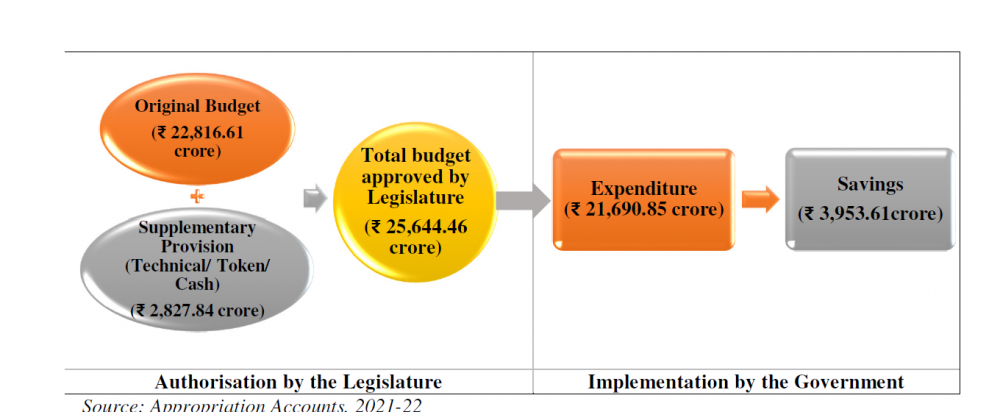

Chart showing various components of budget including appropriation, supplementary grant, re-appropriation. As per the CAG, the above Chart indicates that Supplementary Grant of Rs 2,827.84 crore was not required as the gross expenditure was Rs 1,125.76 crore less than the Original Provisions. (Image Courtesy: CAG)

Morung Express News

Dimapur | March 29

The budgetary management or rather ‘poor financial management’ was under huge scrutiny once again in the latest State Finances Audit Report of the Comptroller and Auditor General (GAG) of India relating to the Government of Nagaland for the year ended March 31, 2022.

As per the report tabled in the Nagaland Legislative Assembly (NLA) on March 28, during 2021-22, against the total budget approved by the State Legislature of Rs 25,644.46 crore (Original: Rs 22,816.61 crore plus Supplementary: Rs 2,827.84 crore), Departments incurred an expenditure of Rs 21,690.85 crore.

This resulted in savings of Rs 3,953.61 crore or 15.42% of the total budget.

“It is indicative that the Supplementary Grant of Rs 2,827.84 crore was not required as the gross expenditure was Rs 1,125.76 crore less than the Original Provisions,” the CAG noted.

Meanwhile, the CAG underscored that the Supplementary Grant was taken on March 22, 2022 though the total expenditure as on February 2022 was only Rs18,504.22 crore as per monthly civil accounts submitted by the Treasuries.

This left Rs 4,312.39 crore with the State Government for the remaining 31 days, it added.

With the Supplementary Grant, total funds available with the State Government were Rs 7,140.23 crore.

According to the CAG, such scenario is indicative of over-estimation and poor financial management.

Further, an expenditure of Rs 0.35 crore was incurred without budget provision which is violative of financial regulations as well as the will of the Legislature, it highlighted.

Accordingly, Supplementary Grants/ Appropriations were obtained without adequate justification, and funds were expended without budgetary provision, the CAG observed.

Despite flagging this issue every year over the last several years, the State Government had failed to take corrective measures in this regard, it added.

There was an overall savings of Rs 3,953.61 crore which was 15% of total Grants/ Appropriations and 18% of the expenditure.

These savings may be seen in the context of estimation of receipts of Rs 22,451.28 crore by the State Government and estimation on the expenditure side being Rss 25,644.46 crore during the year 2021-22.

This implied that the savings were notional, as the funds were not actually available for expenditure, it added.

Meanwhile, at the beginning of the year 2021-22, there was an outstanding excess expenditure of Rs 213.95 crore under 22 Grants (pertaining to the year 2017-18 to 2020-21) which requires regularisation as per the Article 205 of the Constitution of India, the CAG said.

In its recommendations, the CAG advised the Finance Department to provide supplementary grants only after proper scrutiny and realistic assessment of requirements of the concerned Departments, to avoid under or over spending by them.

Departments, which had incurred excess expenditure persistently, should be identified to closely monitor their progressive expenditure and advised to seek supplementary grants/ re-appropriations in time, it said.

Excess expenditure pending regularisation may be regularised by obtaining legislative approval, it added.